Tax Free Savings: An Easy Way To Increase Your Savings

You have decided you are fed up with livin’ la Vida Broka and want to start saving. Maybe you want to travel more or buy your own house. Then you discover your hard-earned savings may be taxed and want to throw a sharp object at someone. Fret not, here is your guide to tax free savings, its legitimate, legal and backed by the government!

If you want to know how to increase your savings, these articles can get you started.

Master the Art of Saving with these 10 Strategies

How To Save Money From A Small Salary – 2022 Guide

Effective Money Saving Tips so You Can Travel Longer

How To Reduce Credit Card Debt By $1,000

How To Reduce Your Mortgage By $80,000

A Tax-Free Savings Account : What is it?

Quite simply, a savings account you don’t pay tax on. When you place money in a savings account, you earn interest on your savings. However, interest on savings can be classified as ‘income’ and can be taxed. The same way you’re your salary is considered an ‘income’ and is taxed.

Saving money in tax free accounts means the government won’t tax that interest income. They go by many names.

In the UK it’s called an Individual Savings Account ‘ISA’, in Canada it is called the Tax Free Savings Account (TFSA), in NZ, The Portfolio Investment Entity ‘PIE’, in Ireland the An Post State Savings and in the USA, the ROTH IRA.

Tax free savings in the UK

Each year, the government allows you to save up to a maximum of £20,000 per year (for 2019/20) tax free, in an ISA.There are four types of ISAs and you can choose to split your allowance between either one of these four ISA accounts.

Individual savings accounts ‘ISAs’

- Cash ISAs- Instant and fixed.

- Lifetime ISAs.

- Innovative finance ISAs.

- Stocks and shares ISAs.

1.Cash ISAs

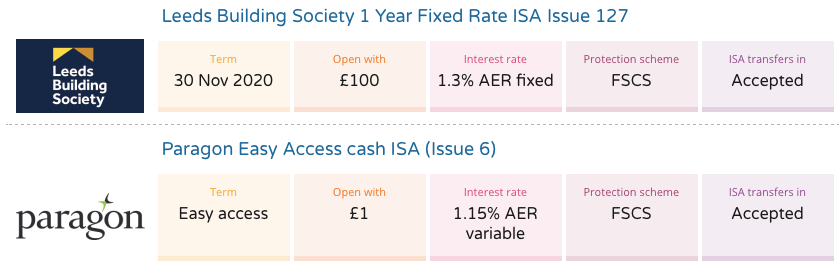

Cash ISAs are savings accounts where the interest is NEVER taxed. Most banks provide them and the savings rate is normally advertised. You don’t have to pay to open an ISA and there are two main types, fixed and instant access ISAs.

The instant access ISA pays a lower rate because you can access your money anytime.

Instant access cash ISA

This allows you to earn a bit of interest on your savings, tax-free, without locking your money away for a period of time. This is a good account if you want to save but aren’t sure if you may need your money in the next few months.

Fixed-term cash ISA

The fixed term cash ISA may also go by the name of a Fixed Rate Cash ISA. You will earn a higher your rate on your savings, but you need to lock your money away for some time. Heavy penalties will be imposed if you withdraw your money before the fixed period agreed is up.

Note* by law, cash ISAs MUST allow you access to your money, even if it’s in a fixed terms savings account, you will just have to pay a heavy penalty.

2.Lifetime ISAs

The Lifetime ISA (LISA) allows you to save up to £4,000 every year tax-free, towards your first home. The best part is, the government will add a 25% bonus to your savings,up to a maximum of £1,000 per year.

This means that if you save £4,000, the government will add £1,000, and if you save £2,000, you will have £2,500. You will also earn interest on whatever you save, and it will also be tax free, as it is in an ISA.

- You must be 18 or over but under 40.

- You can put in up to £4,000 each year until you’re 50.

- Never owned property before.

- It is a residential property in the UK that costs up to £450,000.

- You need to have the LISA open for 12 months or more to use it for a home.

3. Innovative finance ISAs

This type of ISA is for people who have invested in alternative investments such as peer-to-peer lending, crowdfunding, etc. Any interest you earn from these types of loans can be tax free if you open an innovative finance ISA.

It is important to note that this is riskier than placing your money in a cash ISA as the borrower may not pay the loan back.

4.Stocks and shares ISAs

When you trade stocks and shares, you may be taxed on the profit. So, the stocks and shares ISA allows you to invest in funds in a tax-efficient way. Stocks & shares ISAs are typically managed by an online broker or platform who will probably charge you a fee to open and hold a stocks & shares ISA.

Tax free savings accounts in the US

The ROTH IRA

A ROTH IRA is designed to be a retirement plan. It is a great way to earn tax-free interest on your savings. The interest you earn on your savings will not be taxed when the money is withdrawn. It is important to note that the money you invest in a Roth IRA is taxed before you deposit it, but the interest will not be taxed when the money is withdrawn for retirement.

Why does this matter?

If you think you are going to be on a higher income bracket when you are older, it allows you to pay tax when you are on a lower income, instead of later, when you withdraw the funds at retirement age.

- You also need to have had the account for five years before the first withdrawal to avoid a tax payment.

- You can withdraw the money you put into the Roth IRA initially (but not the interest it earned) without penalty.

- You can make small contributions over the year, or contribute one lump sum, as long as your contributions don’t exceed $6,000 ($7,000 if you’re 50 or older).

Health saving accounts

A Health Savings Account (HSA) is created for individuals who have a high-deductible* health plan (HDHP)* and helps cover qualified medical expenses. Contributions are tax-deductible, the income that grows is tax free and withdrawals are tax free too.

- You must participate in a high-deductible health plan (HDHP).

- Annual contributions are limited to $3,450 if you have individual HDHP coverage and $6,900 if you have family HDHP coverage.

- It does not require an employer sponsor.

- You don’t lose your money if you don’t spend it and can be rolled over year to year.

- It can serve as an extra source of retirement savings if you don’t spend it.

- It can earn interest.

- It can only be spent on qualifying health-related expenses.

*A deductible is a portion of an insurance claim you need to pay if you want to make a claim. If you are part of a high-deductible insurance plan, you pay a higher deductible amount than typical health plans.

For example, if you had a deductible of $2000 and make a medical claim for $5,000, you would have to pay $2,000, since the insurer is only responsible for the excess, which is $3,000.

Flexible Spending Accounts

A FSA allows money to be contributed, grown and withdrawn without taxes. The account allows employees to contribute some of their earnings to pay for qualified medical expenses and childcare expenses. It is important to note that only $500 can be rolled over into the next year and any unused money is forfeited.

- Are set up by an employer for an employee.

- Employee contributions are limited to $2,650 per year

- Employers can supplement employee contributions to them.

- It must be set up with an amount that is declared at the start of the year and cannot be changed.

- It doesn’t require that you have a high-deductible health insurance plan.

Do you know any other ways to reduce your tax bill? Please share it in the comments below!

If you are looking for other ways to make extra money, it’s worth reading these :

25 Quick Ways to Make Extra Money

21 Frugal Living Tips To Payoff Your Debt

How To Make $1,000 FAST: 6 Simple Tips